3 Different Types of 1940 Act Funds

The Investment Company Act of 1940, which defines the landscape for retail investment products recently turned 80 years old. Tender offer funds and Interval funds are increasingly popular structures that fit into this category but they are only one part of a much broader landscape. Lets take a closer look at the different types of funds that retail investors can access under the protection of the 1940 Act.

Fund Types Regulated

The universe of 1940 act funds is broad and deep, encompassing almost any type of investment strategy, provided it can comply with the transparency and corporate governance standards of the rule. Broadly speaking there are three types of funds covered by the 40 act: Open end funds, closed end funds, and unit investment trusts.

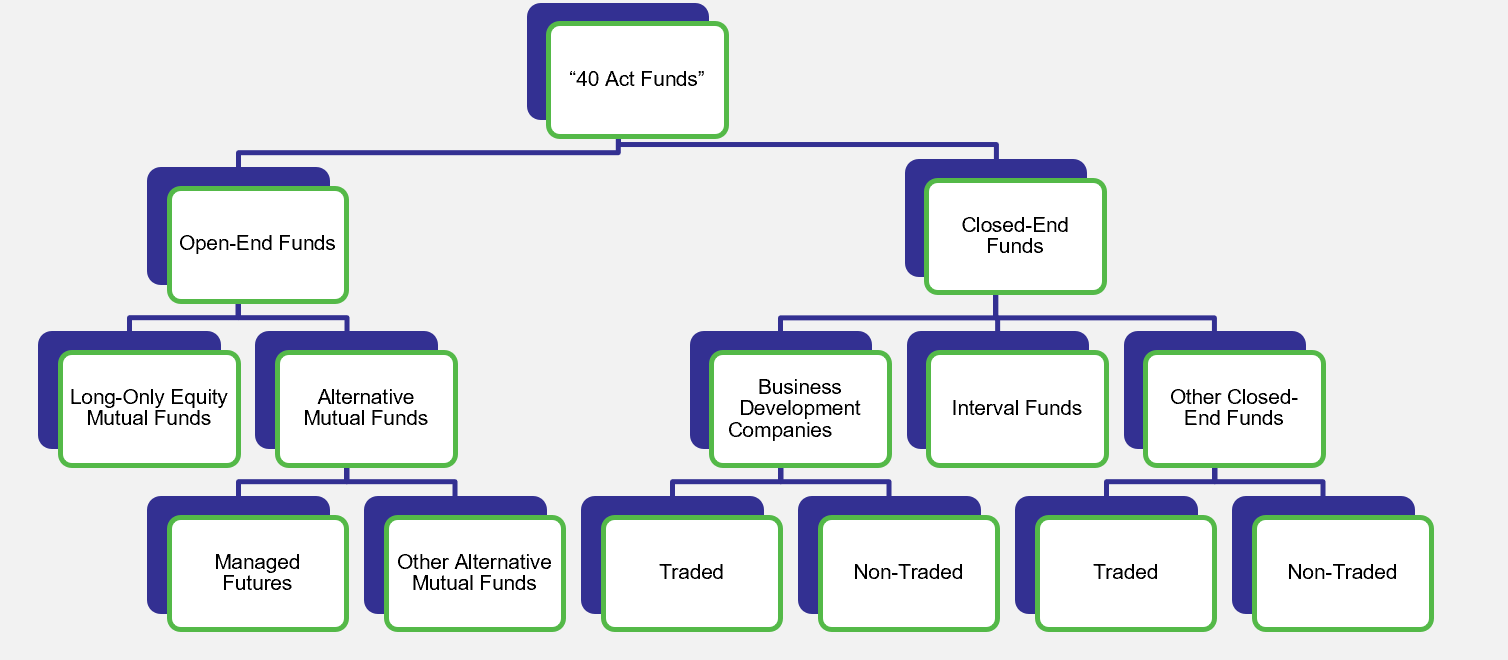

This picture summarizes the different types of open end and closed end funds:

Unit investment trusts offer fixed portfolios as redeemable units, and are typically only active for a fixed period of time. UITs have no board of directors. Most investors have limited experience with UITs, but are more familiar with actively managed open and closed end funds.

Open end funds, commonly known a mutual funds provide daily liquidity to investors. Most investors use open end funds to get exposure to long only equity funds. There are also alternative funds that ofer more excotic strategies. Managed futures are the most popular type of alternative mutual fund. There are othe mutual funds that offer exposure to hedge funds as well.

Closed end funds do not have to offer daily liquidity to investors. As a result they have much greater flexibility to pursue different investment strategies. Business development companies are technically a type of closed end funds that are required to provide capital to small and medium sized enterprises. They were originally designed to be a vehicle to provide venture capital to the masses, but over time they have focused primarily on credit strategies, and are used as income vehicles.

There are also over 600 closed end funds in the market. Most of these funds conduct one time IPOs, then are traded on an exchange. Traded closed end funds are well covered by sites such as CEF Connect and Seeking Alpha. Our affiliate covers traded closed end funds here. Most traded closed end funds follow relatively traditional investment strategies. However, in recent years, more investors have been seeking out alternative investments. Unlisted closed end funds are the best vehicle for investors who want to access alternative strategies. Unlisted closed end funds used to be opaque. Yet, Ockham Data has launched a network of websites(including this one) in order to make the unlisted closed end fund market more transparent.

There are two types of unlisted closed end fund: tender offer funds and interval funds. Both types offer many key advantages including exposure to hard to access managers, convenient tax reporting and transparency. Yet there are several subtle differences, which we outlined in a previous post. The most important difference relates to repurchase plans. Interval funds can only change their repurchase plans with shareholder approval. In contrast, boards of tender offer funds can change repurchase plans more easily. There are tradeoffs between these two structures, which fund sponsors and investors should consider before making decisions.